Product · Autonomous Credit Intelligence Platform

The AI-native brain for advance cash-flow

underwriting.

ACIP is an AI-native, multi-agent mesh orchestrated by LangGraph for advance cash-flow underwriting and macro-economic risk analysis, replacing legacy static credit scoring with dynamic, receivables-based intelligence.

Advance Cash Flow Underwriting

Underwriting forward-looking liquidity

Legacy scoring looks 60-90 days backward at stale FICO and Paydex data. ACIP evaluates a business’s forward-looking liquidity by analyzing the quality and velocity of its accounts receivable: how fast invoices convert to cash, and how reliably.

- AR velocity analysis: Measures how quickly receivables turn into deposited cash.

- Real-time, not stale: Decisions reflect this month’s liquidity, not last quarter’s.

- TEE-backed security: Underwriting runs in a Trusted Execution Environment with attested outputs.

The Mesh

Six specialized agents, one decision

Orchestrated by LangGraph, each agent owns a slice of the underwriting problem and hands off through a shared state graph.

Ingestor

Pulls Nav, Plaid & Rental Kharma data through Skyflow vaults

RTCFA Engine

Quantitative Real-Time Cash Flow Analysis of AR velocity

Borrowing Base

Computes eligible AR and net advance rate in real time

Skeptic

Adversarial fraud detection across cash-flow patterns

Macro-Risk

Sector liquidity & macro-economic risk overlay

Orchestrator

LangGraph mesh coordinator · TEE-attested decisions

The Borrowing Base Model

Transparent underwriting math

Our fundable credit line is defined by a clear, auditable chain of formulas. Hover any card to inspect it.

Ineligible = 90+ day past-due, concentration excess, and cross-aged receivables.

A base rate of 85% is eroded by reserves that price in receivable risk.

Legacy To Next-Gen Transition

Visualizing the ACIP Stack

The Autonomous Credit Intelligence Platform (ACIP) replaces manual, delayed risk analysis with an interconnected, real-time data ecosystem. Below is an overview of how our proprietary engine operates.

1. The Modern Underwriting Ecosystem

The holistic architecture bridging Guapaholics white-label issuance with the ACIP Intelligence Platform. The transition from legacy systems relies on automating the ingestion of robust data points directly into a decentralized, TEE-attested processing engine.

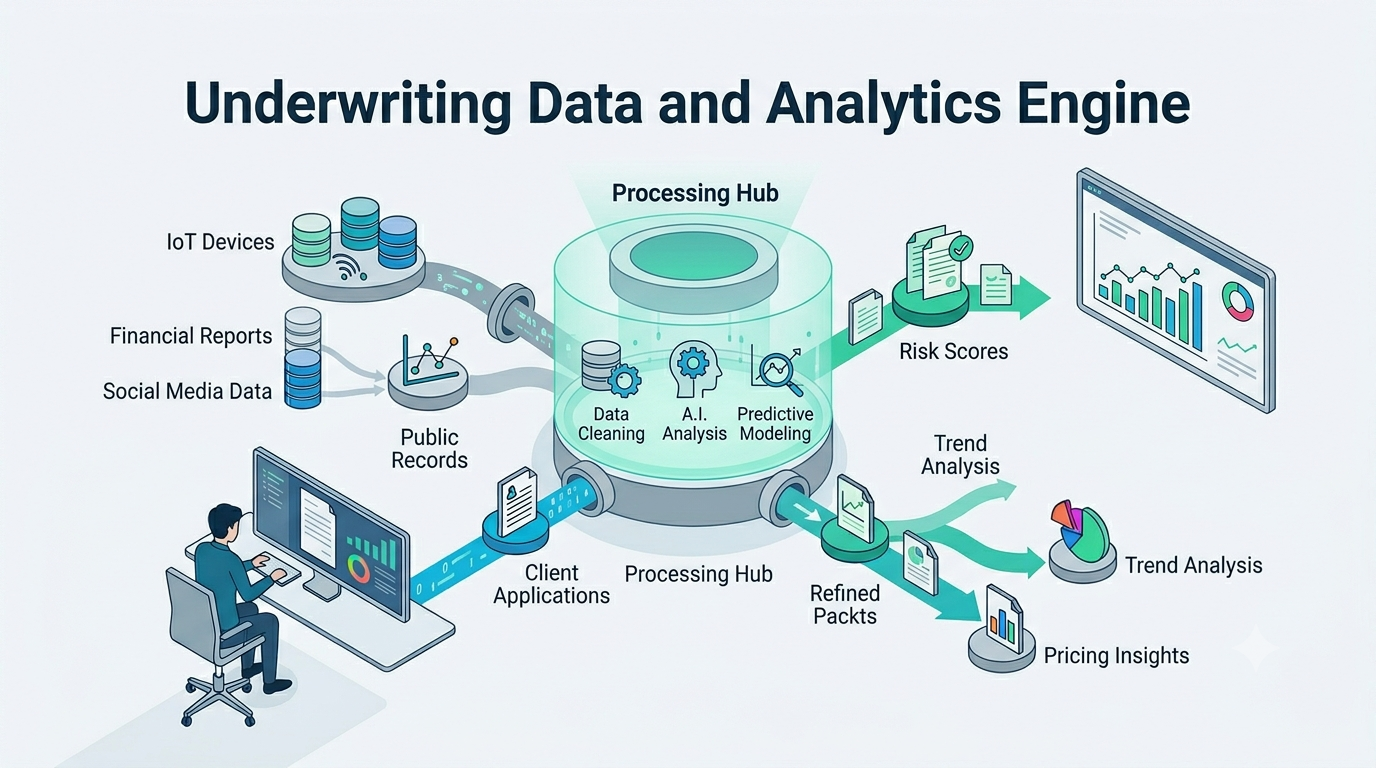

2. Deep Dive: The Data and Analytics Engine

Unlike legacy manual underwriting, ACIP's Data & Analytics Engine actively pulls continuous real-time data streams, with heavy emphasis on strategic partnerships with NAV, Plaid, and Rental Kharma data through Skyflow vaults. The core engine applies automated predictive modeling, cleaning, and normalization to fuel our LangGraph orchestration mesh.

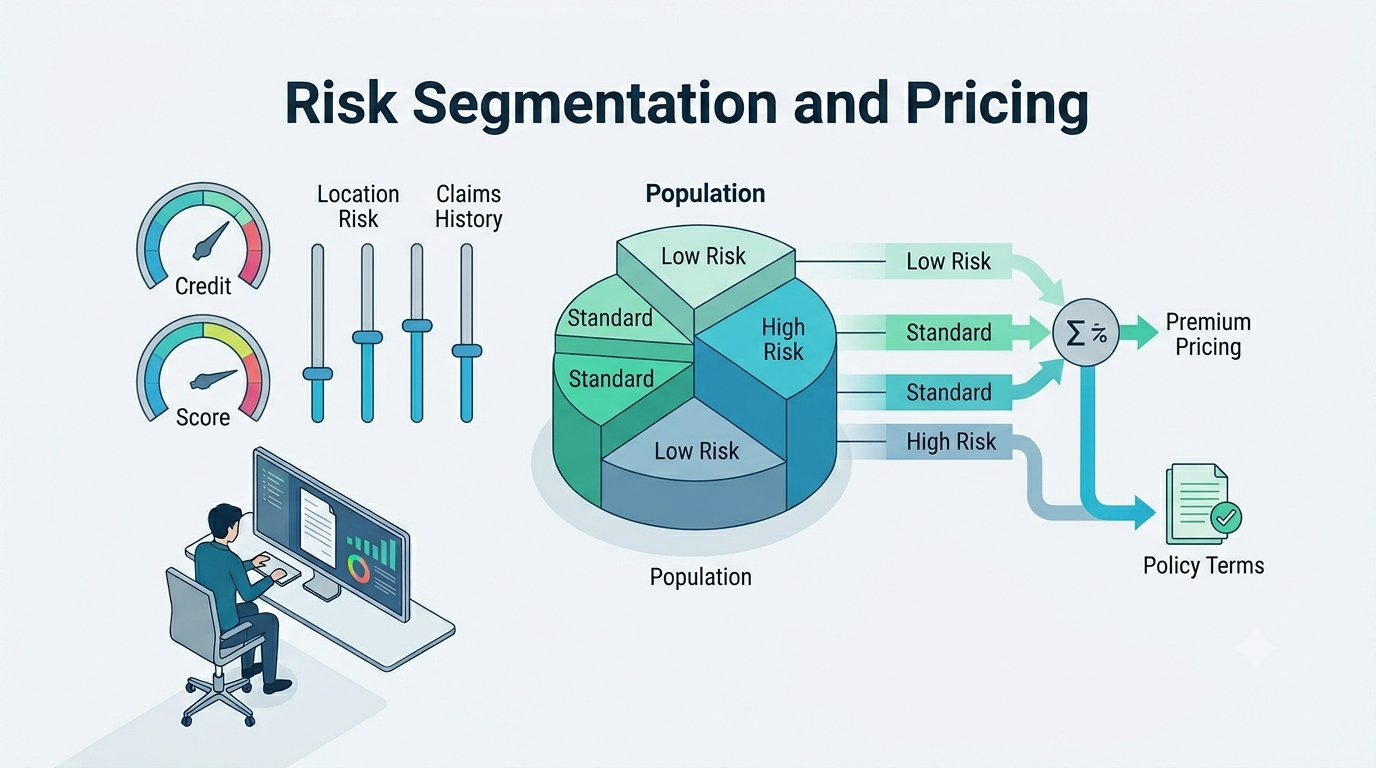

3. Core Process: Risk Segmentation and Pricing Models

By moving away from static, point-in-time scoring, ACIP leverages the refined engine outputs to dynamically manage core business decisions. Our Skeptic Agent evaluates risks on a continuous spectrum, establishing discrete segmentations, dictating precise premium pricing, exact policy terms, and calculating net advance rates in real time.

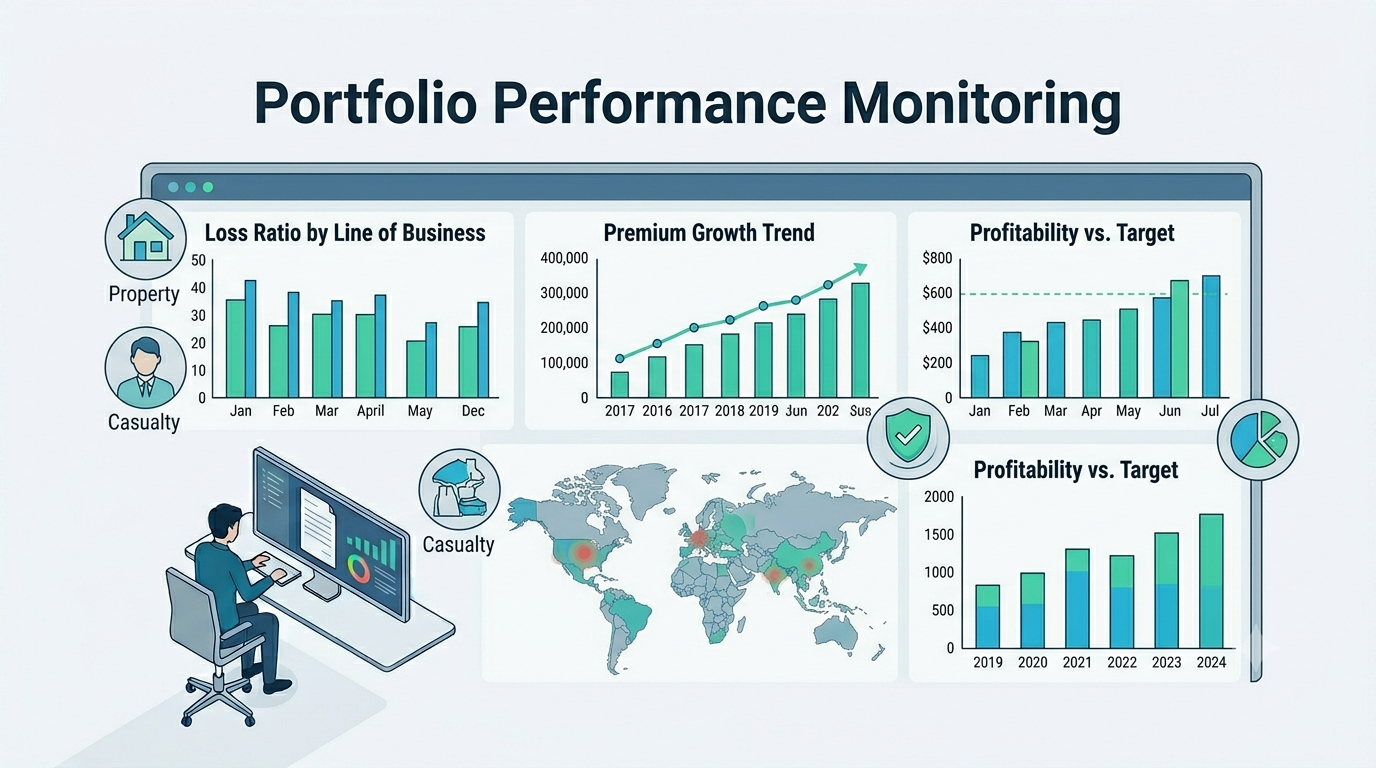

4. Outcome & Management: Portfolio Performance Monitoring

Completing the loop, the ACIP Intelligence Platform provisions advanced executive dashboards. Tracking Key Risk Metrics, like Loss Ratios across lines of business, premium growth trends, and geographical risk concentration, allowing CDFIs to manage aggregated underwriting data to achieve profitable, mission-driven growth.

Key Risk Metrics

What ACIP computes on every facility

| Metric | Definition | Formula | Threshold |

|---|---|---|---|

| DSCR | Debt Service Coverage Ratio | EBITDA ÷ Annual Debt Service | ≥ 1.25× |

| DSO | Days Sales Outstanding | (AR ÷ Monthly Revenue) × 30 | ≤ 60 days |

| CCC | Cash Conversion Cycle | DSO + DIO − DPO | Flag if > 90d |

| Dilution Rate | AR erosion | (Write-offs + Credits) ÷ Gross AR | Drives reserve |

| Advance Rate | Net funding rate | Base 85% − Reserves | Applied to eligible AR |

| Velocity Score | Throughput composite | Net CF ÷ (Debt Svc × Revenue) | 0 - 1 composite |

Adversarial cash-flow fraud detection

A dedicated agent is trained to assume the books are lying, surfacing six sophisticated fraud patterns before capital moves.

Circular Cash Flow

Money cycling between related entities to artificially inflate accounts receivable.

Advance Rate Squeeze

AR quality quietly deteriorating mid-facility as DSO and dilution creep upward.

Debt Stacking

Multiple lenders advancing against the exact same pool of receivables.

Concentration Gaming

Keeping a single customer’s share engineered just below the 25% cap.

Synthetic Revenue

Fabricated invoices designed to inflate the borrowing base.

Seasonal Masking

Applying at peak season to deliberately hide trough-season cash flow.

Underwriting that thinks like an analyst

Pair ACIP with Guap Finance issuance for a fully autonomous, white-label lending stack built for CDFIs.